July 31, 2026

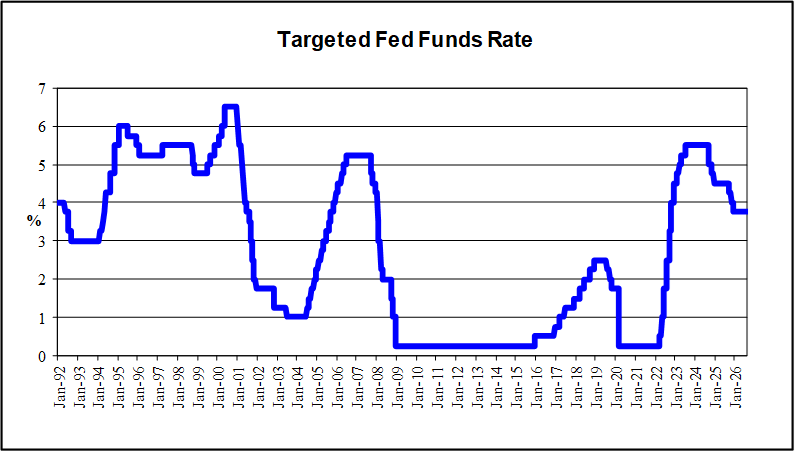

With the U.S. economy continuing to move forward, helped by a resilient consumer and labor market conditions that appear to have stabilized, the Fed is focusing on the inflation side of their dual mandate. In his testimony to the House Financial Services Committee and Senate Banking Committee, Federal Reserve Board Chairman Kevin Warsh emphasized the Fed’s responsibility to stabilize inflation. Also in that testimony, Warsh reiterated his belief that the near term inflationary impact of the Artificial Intelligence (AI) boom would give way to medium term disinflation from the resulting increase in productive capacity, making the case for a short-run-wait-and-see policy. And, that’s what the Federal Open Market Committee (FOMC) did at its July 28-29 meeting.

The decision to hold rates steady was a close call with three Committee members dissenting in favor of raising rates by ¼ percentage point. The policy statement released at the conclusion of the meeting was sparse and ended with, “Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain areas, including energy. The Committee will deliver price stability.” In his post-meeting press conference Fed Chairman Kevin Warsh said the central bank will be watching inflation data in the period ahead and will not hesitate to act as needed. “If inflation stays high, rates could be part of the solution.“

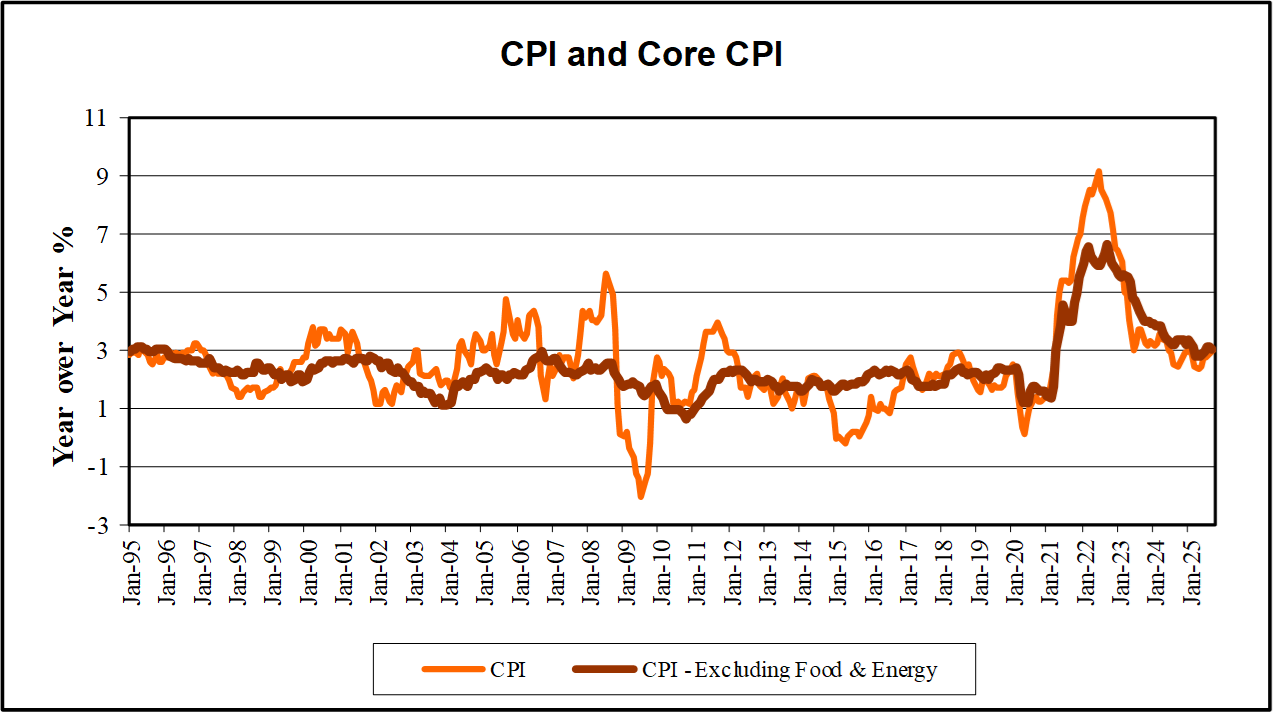

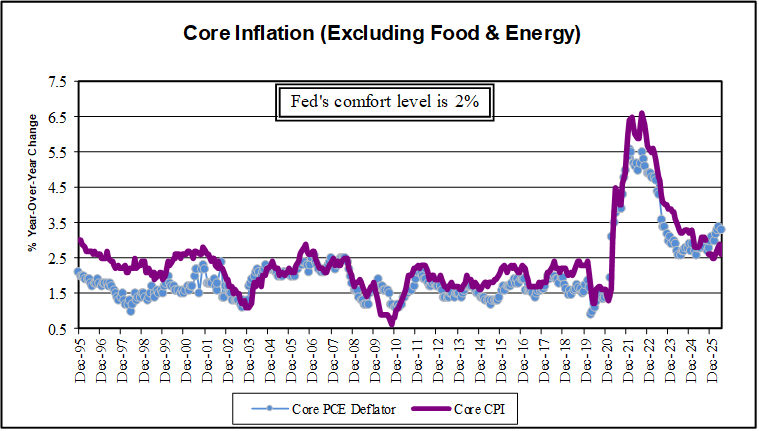

There are three (3) inflationary forces that have put the Fed on high alert: tariffs, AI investment and energy prices. June’s inflation gauges were seen as largely benign. The Consumer Price Index (CPI) headed in the right direction in June due to the monthly drop in global crude oil prices. Headline CPI fell 0.4% month-on-month, the largest one-month decline since April 2020. On a twelve-month basis, CPI stepped down to 3.5% from 4.2% in May. Core (excluding food & energy) CPI, on year-over-year basis, posted the slowest pace since before the U.S. – Iran conflict at 2.6%, down from 2.9% the prior month. Producer prices were also softer than expected. PCE Deflators also eased on June to 3.7% for headline and to core’s 3.3% year-over-year rates. Still, these inflation levels are too high, and renewed oil shock on the escalation and widening of the Middle East conflict and threats of new tariffs may re-ignite price pressures going forward.

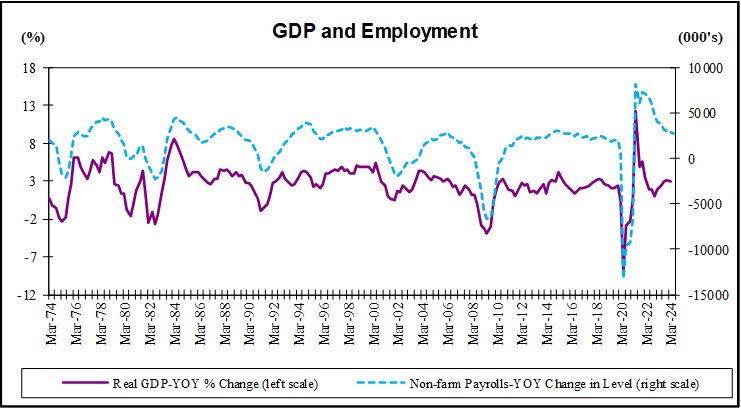

The job market stumbled a bit in June, and the prior two months saw some downward revisions. Payrolls moderated with the number of jobs added lower than anticipated. On the other hand, the unemployment rate ticked lower to 4.2%, its lowest level in a year, but the decline was attributed to a plunge in the labor force that was larger than the drop in employment in the household survey. Other indicators of labor conditions were mixed as initial and continuing claims for unemployment benefits have been trending lower. Meanwhile, the 4-week moving average of private employment increases provided by ADP has also been trending lower. Taken together, it appears that the low hire-low fire environment remains, suggesting labor conditions are in balance, even as consumers are concerned about job availability according to outlook surveys, such as the Conference Boards Consumer Confidence Index and the University of Michigan Consumer Sentiment Index.

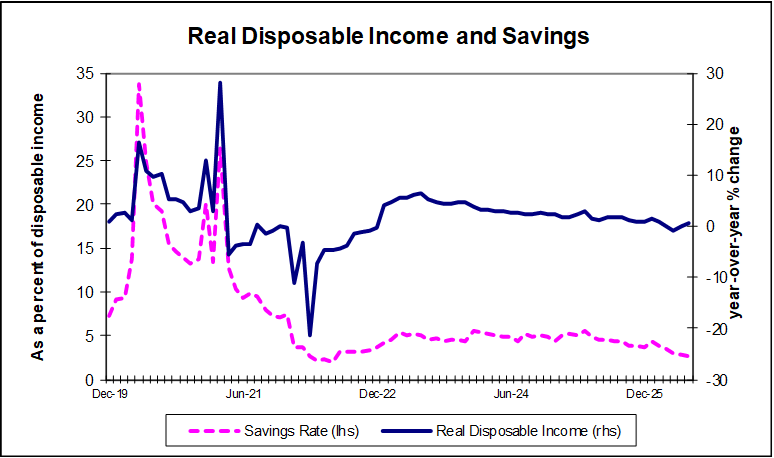

To date, the consumer has shown reliance, but household spending may be losing momentum. Shoppers pulled back on spending in June. Retail sales rose just +0.2% in the month, the weakest print since January, even as total sales were boosted by Amazon Prime Day and Walmart’s online sales events. With higher tax refunds mostly exhausted, weak disposable income and tapped out savings, some slowdown in real consumer spending should be anticipated.

The ever-evolving conflict in the Middle East is making for a volatile energy market and additional global tariff levels proposed by the Administration complicates the U.S.’s economic outlook, and in turn, the Fed’s task. Market-based inflation expectations have only moved slightly higher and are significantly lower than a year ago. The Fed is also awaiting the findings from the five task forces, providing some additional basis for staying patient. A prolonged war and new tariffs could, however, have wide-ranging consequences, especially to lower-income Americans and small businesses. With inflation remaining elevated due to geo-politics, AI driven demand and tariffs, plus Fed officials warning that a more restrictive policy rate may be needed to counter persistent inflation, a rate increase by year-end remains on the table. In fact, the financial markets still believe it is an odds-on bet, but incoming data and developing beliefs regarding the impact of AI on inflation, near-term and long-term, will dictate the Fed’s ultimate path.

Full Fusion

Full Fusion