![]() Main Menu | Adv. Income Shock | Assumptions | Index Rates

Main Menu | Adv. Income Shock | Assumptions | Index Rates

When the assumptions to be made are some form of rate assumptions, additional interface features are available.

These features are available in the following assumption interfaces:

Advanced Shock Income |

- Index Rates, Reinvestment Rates |

Advanced Economic Value of Equity (EVE) |

- Index Rates, Discount Rates |

Base Index

Any rate assumption can be based upon a specific index. Changes in the index will flow automatically to assumptions based on the base index. This will save time updating your rates. This only applies to Spreads and Volatility. It does not apply to the Value option. If you have entered rates based on the Value option, the rates will not change, you will need to manually review and change those rates.

The indices available for the base index are those that have been setup, i.e. have been provided with rate assumptions in the various scenarios, under the Index Rate section.

Select from list of indices in the Base Index drop-down box. This causes the effective rates for this index to be placed in the Base column of the rate assumption grid.

Rate Assumption Methods

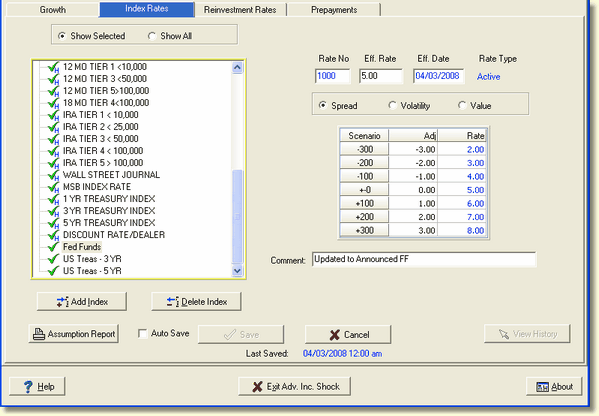

The system uses three methods to set the index assumptions; Spread, Volatility, and Value.

Spread

This is the default method when a Base Index is selected. The values entered into the Adj. column of the rate assumption grid are considered a spread in percentages that are added to the Base index to derive at the final rate used as the assumption. This rate is displayed in the Rate column of the rate assumption grid.

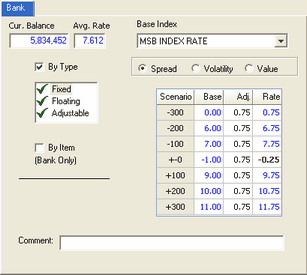

When the Spread radio button is selected the screen below is displayed. Using an example of "Fed Funds" the spreads are keyed as shown below.

Adj. Column - This is an input column. The number that you input in this column will become the spread in relationship to the effective rate, which in the example above is 5.00%. The adjustment the user enters will be rounded to two decimal places.

Rate Column -This column will illustrate the effect of using the spread that you input on the index. It is a "read-only" line; you cannot input directly to any of the cells in the Rate column.

For instance, if the effective rate for Fed Funds falls 50 basis points to 4.50% the next time data capture is performed, the system will keep the same -3.00 spread under the "-300 rate shock" environment, and will recalculate the rate in that case to be 1.50%. Unless you have a need to change the spread relationships, there will thus be no need to re-enter any data.

For indices that you have set up manually, the Eff. Rate field can be edited in order to alter the current rate for that index. Like the indices originating from your host system, the spread assumptions for manual indices will be "remembered" and the rate assumption in each of the shock scenarios will be recalculated based on changes you make to the effective rate.

One of the efficiencies of the IRR system is that it "remembers" these inputs. In other words, the spreads that you input will remain in effect until you change them, even if the effective rate coming from the host system changes.

When using the spread method, the possibility exists that negative rates are created if the host rates dropped from one month to the next and the spread was not adjusted. This can easily happen in the Deposit rate indices, since their values are relatively low already.

The system will highlight such a condition by showing the final negative rate in red. See the subheading No Rate Assumption and Negative Rates below for an explanation of the system defaults.

If the user chooses not to specify a reinvestment rate, the system will utilize the accounts weighted average rate, calculated from the underlying runoff, to reinvest each portion of the reinvestment amount with its own weighted average rate.

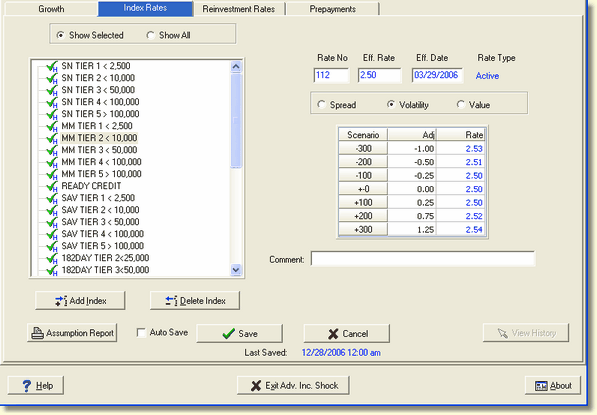

Volatility

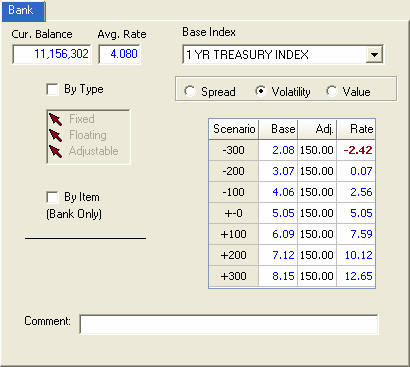

If you want to assume that the index will move as a "percentage" of the Shock scenario from its current effective rate as market rates change, use the Volatility method, as illustrated below.

The example index rate above is the MM Tier 2 <10,000 index. Rates related to demand or transaction accounts rarely move with the same frequency or to the same degree as the fed funds rate.

For instance, if the fed funds rate goes up 50 basis points, you probably will not move your rate on Money Market accounts up 50 basis points every time. It might be more realistic to use a percentage to set these kinds of indices in a rate shock environment.

When market rates come down 300 basis points, we might assume that the MM Tier 2 <10,000 rate will only change by 30% of the market move. 30% of 300 basis points equals 90 basis points which is subtracted from the current rate to arrive at the final rate of 1.60%. (This assumption is for demonstration purposes only. Such an assumption will vary with every institution, and should be based upon a consideration of many factors, such as how this rate has been set in the past under similar circumstances, the net interest spread the institution would need to maintain in such a circumstance, and how depositors might respond to such an approach to pricing, to name a few.)

As we noted, your institution may have a greater or lesser correlation to the Fed Funds rate than shown here for a similar index.

To assume that the index will not change in a "no change" environment, 0% is entered. But you might expect, perhaps in an extremely competitive deposit market, greater responsiveness in the NOW 1000 index as rates rise.

As in the "Spread" method, the system will retain the volatility assumptions to be used in the future, even when the current effective rate changes.

In the example above, if the current effective rate falls to 1.95% and you make no changes to the volatility, the rate used under "-300" will change to 1.05% ( 1.95% - (300 * 30%) ).

And if the index is a manually created index, you can change the rate in the Eff. Rate field to make any adjustments to the current rate that you wish, and the system will adjust the figures on the Rate column based on the percentage in the Adj. column.

Values entered are numbers greater than 1. Percentage values above 100% are allowed. The adjustment the user enters will be rounded to two decimal places.

In the volatility method, the values entered are a percentage of the shock scenarios by which the base rate of the index is added to derive at the final rate assumption. Changes in the base rate will automatically reflect in the actual rate being applied.

Following is the calculation the system does to arrive at the rate.

Shock Scenario |

Adj. |

|

Base Rate |

|

Final Rate |

|||

-.300 |

X |

150.00 |

= |

-4.500 |

+ |

2.08 |

= |

-2.42 |

-.200 |

X |

150.00 |

= |

-3.000 |

+ |

3.07 |

= |

0.07 |

-.100 |

X |

150.00 |

= |

-1.500 |

+ |

4.06 |

= |

2.56 |

0 |

X |

150.00 |

= |

0.000 |

+ |

5.05 |

= |

5.05 |

+.100 |

X |

150.00 |

= |

1.500 |

+ |

6.09 |

= |

7.59 |

+.200 |

X |

150.00 |

= |

3.000 |

+ |

7.12 |

= |

10.12 |

+.300 |

X |

150.00 |

= |

4.500 |

+ |

8.15 |

= |

12.65 |

An example of this is shown below. Here the result rate is 150% of the 1 Year Treasury index.

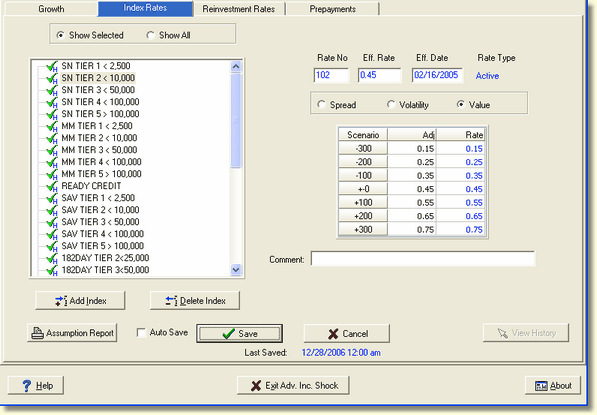

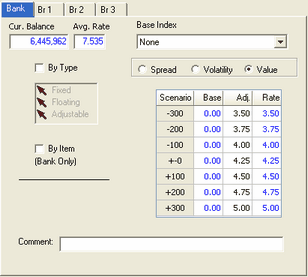

Value

This method assumes no relationship necessarily between the rates in each of the shock scenarios and the current effective rate. Rather, it allows you to input the actual rate into each of the shock scenarios.

To enter the rate assumption itself, rather than using a Spread or Volatility method, select the Value radio button.

Using the Value method, the number in the Rate column changes to the same number that you entered in the Adj. column. The adjustment the user enters will be rounded to two decimal places.

As with the other methods, the system will remember the assumptions you make under the Value method and will retain them even when the current effective rate changes, either due to changes in the rates coming from the host system or to changes you make to the effective rate on indices that you have set up manually.

While this "memory" contributes to efficiency, it also makes it important to review these assumptions on a periodic basis. This is why the check mark-![]() , preceding the index in the display will change to a question mark-

, preceding the index in the display will change to a question mark-![]() , if the particular assumption has not been updated in three months.

, if the particular assumption has not been updated in three months.

When the value option is selected as the basis for assumptions, in the Reinvestment Rates or Discount Rates tabs, the Base Index will be automatically defaulted to "None". The base rate therefore is zero, and the values keyed into the Adj. column of the assumption grid also represent the final assumption rates. This method would typically be used when the rate to be applied does not have any correlation to a driver rate.

Note however, that the appropriateness of the rates used should be reviewed periodically.

![]()

No Rate Assumption

No rate assumption on the account will default to a reinvestment rate equal to the average rate on the account (for interest bearing accounts).

Negative Rates

If assumptions entered by the user would result in negative rate assumptions to be applied, the system automatically changes those assumptions to .01 rate during processing.

A visual highlight to the rates grids has been added to make negative and zero rates more visible to the user. If the resulting rates are negative or zero, they will be in Bold & Red. This can happen in the declining rate environment where the host rates have dropped and the existing spread or percentage causes a negative or zero final rate. See the screen below: