Some of your institution's indices may move parallel to general market rates but you need the flexibility to change those indices which do not move parallel. IRR-Solutions® II gives you the flexibility to set your indices based on circumstances within your institution.

The process of making Index rate assumptions involves determining what the index in question would be pricing at under the various shock scenarios. For some indices such as Prime Rate or an In-house prime, this means in parallel with Fed Funds rate, which is the assumed underlying proxy for the shock simulation. For others, the assumed rates in the various shock scenarios will either lag behind the assumed changes in the Fed Funds rate or be more or less static.

The following examples will explore possible rationales for making assumptions. In all the other "Setting assumptions" area of this manual, these examples should not be taken verbatim, but only as examples of the thought process applied in deriving the assumptions.

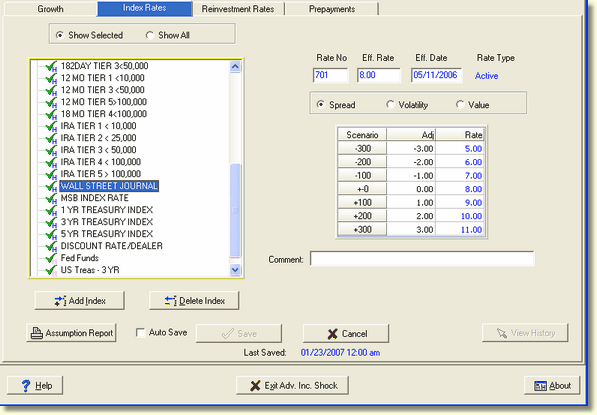

Parallel Assumptions

A typical setup would be the one shown above, where we defined a spread equal to the shock rate in each scenario.

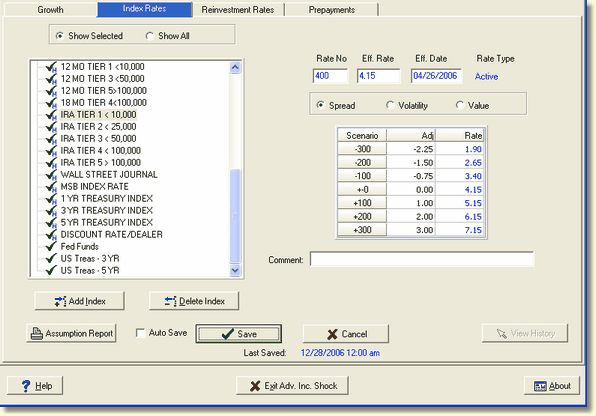

Lagging Assumptions

Many times an institution's pricing will lag behind market rates in declining rate scenarios, and either lag less or follow market rates in the rising scenario.

In the example shown here for pricing variable rate IRA's, pricing increasingly lags behind the market pricing in the down rate scenarios, but follows the market rising rate scenarios in parallel.

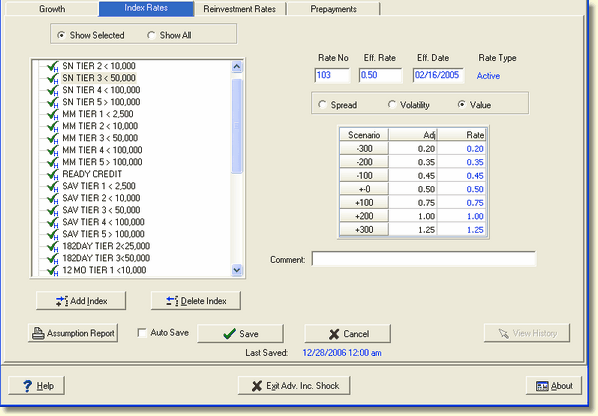

Independent Assumptions

In an institution's deposit area, pricing in the various rate scenarios is largely independent of the market rate environment and tends to stay relative static with regards to market rate changes.

Now accounts are typical examples of such pricing. Pricing in these accounts in the various scenarios is more influenced by the customer base in these accounts and the local market, main market rates. As you can see in the example above, rate assumptions change less than 100 basis points in either direction for a 300 basis point change in the shock scenario.