The most common area where an institution may experience prepayments is in the loan area of the balance sheet. In a declining rate environment, sometimes significant prepayment rates can be experienced based upon the institution's market environment. Borrowers will tend to refinance their loans with the lower rate when rates have dropped significantly enough to offset the fees charged for refinancing and still provide them a future advantage on their loan.

Floating and Adjustable rate loans are typically not affected by this principle, because their rate adjusts either immediately or within a certain periodic interval to the new rate environment.

Most institution's will experience a certain minimum rate of prepayments regardless of the rate environment in their mortgage loans due to the fact that borrowers sell their homes and pay off their mortgage, or make additional payments to speed up the payoff of their mortgage.

Based upon the above discussion, we made the following sample prepayment assumptions. Again, just like in all the other "Setting assumptions" areas of this manual, these examples should not be taken verbatim, but only as examples of the thought process applied in deriving at the assumptions.

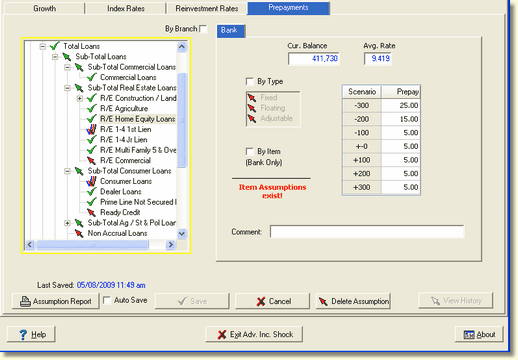

We start out by setting a nominal level of prepayments at the subtotal level Total Loans representing the commonly experienced rate of prepayment regardless of the rate environment.

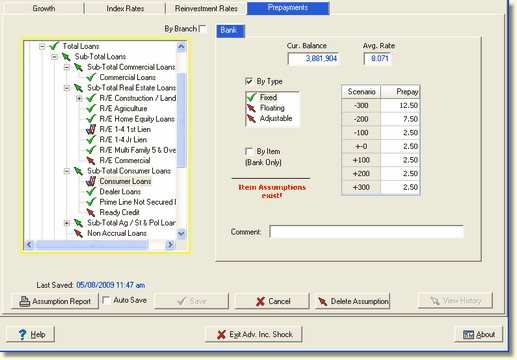

We followed up with setting split type level assumptions for the Consumer Loans account, indicating a higher rate of prepayment in the declining rate environment for the fixed rate portion of the account.

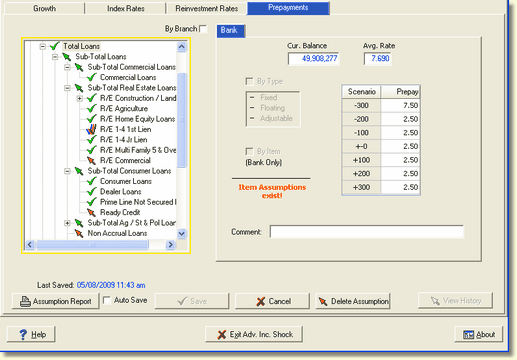

We place the highest level of prepayments on the R/E Home Equity loan account. Using the Account Information Tools, we determined that the account is primarily comprised of fixed rate loans, therefore it is not necessary to make split type assumptions.