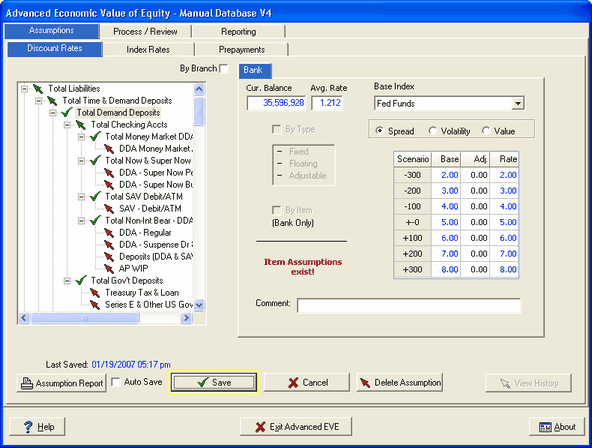

When we come to assigning discount rate assumptions for demand deposits, some different considerations must be taken into account. Intuitively, we understand that these accounts represent one of the most valuable portions of an institution's balance sheet. These are typically very low cost funds or, in the case of non-interest bearing demand deposits, they are "free" funds against which the institution can lend money and usually generate a very handsome spread. Furthermore, these deposits generally represent very stable, "core" funds. Inasmuch as depositors are sacrificing yield in favor of safety and liquidity, as they are able to draw against these accounts, these funds tend to be much less responsive to changes in interest rates than CDs.

From the standpoint of assigning a discount rate for valuation purposes, the problem with demand deposits is this: because of the low rates on these accounts, and their usual low degree of responsiveness to changes in market rates, using their current and projected pricing to arrive at a value will understate their true value to the institution. To use an extreme example to illustrate, consider the basic non-interest bearing demand deposit that, by definition, carries no interest rate. Using a 0% rate to discount the value of the account will yield no gain in value over book, no matter how much rates change! Yet, we know that these accounts are the most valuable accounts to the institution on the liability side of the ledger, particularly in an increasing rate environment.

We resolve this dilemma by using a higher, more "market" driven rate for discounting demand deposits. This is justifiable if we consider the fact that we probably cannot just go out into the market and replace these funds at the same low or zero interest rate. These core deposits are not gathered in the market place in the same way that we can usually go out and gather CDs, by offering competitive rates. Demand deposits usually come to the institution as the result of a marketing process that involves appealing to consumers on the basis of relationship, service, and access. To attract demand deposits purely on the basis of return would probably require offering rates that approach the level of rates offered on CDs.

In setting discount rates for demand deposits, then, we will be thinking in terms of how the institution would price CDs in the respective rate shock environments. Given that, the most efficient approach would be to use an index based on projected CD pricing that we can also use to discount demand deposits. We have already set up such an index. (See "Index Rates" for a discussion on setting up an index manually.) Now, we will tie our demand deposits to the 6 MONTH CD index for discounting purposes as shown below:

The index rates that this system reads from your institution's subsystem will be ones that are tied to accounts whose rates adjust automatically when the index changes. The 6 MONTH CD index exists in the subsystem and is currently 3.45%, but because no floating or adjustable rate accounts are tied to it, it did not get set up automatically in our Index Rate set. We had to set it up manually.

You will notice that the assumptions that we used in setting up the 6 MONTH CD index do not track the shock scenarios on a one-to-one basis. In other words, when the shock scenario goes from +/-0 to +100 (fed funds rate up 100 basis points from the current level), the rate projected on the 6 month CD goes from 3.45% to 3.70%, or 25 basis points.

We anticipate that the institution will be able to "lag" increases in CD pricing behind increases in market rates. The projected lag becomes even greater when the shock scenario goes from +100 to +200, as the rate projected on the 6 month CD goes from 3.95% to 3.95%, or 50 basis points.

Similarly, there is not a one-to-one change in projected CD rates as the shock scenarios decline. These patterns will vary depending upon the institution, its market, and its competition. In some competitive situations, there may be no lag at all as rates rise or fall.

Recalling our discussion from above in regards to loans, for the sake of efficiency, the most effective approach is to set a "general" assumption, usually set at a subtotal level, that will apply to the numerous smaller accounts, knowing that we will then go in and make more specific assumptions for the more significant accounts or items. In the case of demand deposits, we will typically have several large interest-bearing accounts, but numerous smaller non-interest bearing ones. Thus, at the subtotal "Total Demand Deposits", we should make the discount rate assumption that we want to apply to the non-interest bearing accounts.

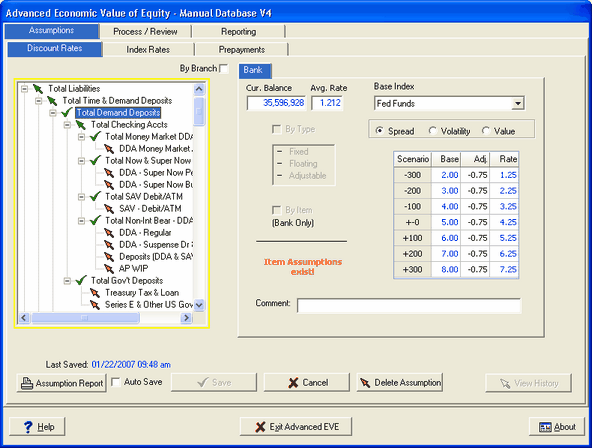

In determining this discount rate for demand deposits, we usually mark down from the CD rate based upon the rate on the demand deposit account and, to a lesser degree, the relative ease with which depositors can draw on the account. For non-interest bearing demand deposits, we generally mark down from the CD rate by 75 basis points, as seen below:

The assumptions that we have entered here will cause all demand deposit accounts, unless overridden by other assumptions that we will enter, to be valued against the 6 month CD rate less 0.75% in the respective rate shock environments. In this particular example, in the "no change" shock environment, a demand deposit would be valued against 2.70% (3.45% - 0.75%).

As long as the rate on the particular demand deposit is currently less than 2.70%, including non-interest bearing deposits, which are priced at 0%, we will have a gain. This is opposite from what we found on the asset side of the ledger and is an important point to keep in mind. Whereas with assets, it was more valuable to us when the current rate on the account was greater than the rate at which the account would reprice, liabilities are more valuable to us when the current rate on the account is less than the rate at which the account would reprice. This is logical: we would like to make more than the prevailing rate on our assets, and we would like to pay less than the prevailing rate on our liabilities.

Let's look at some of the accounts that subtotal into "Total Demand Deposits."

Scrolling down the listing of accounts that subtotal into "Total Demand Deposits," we see that most of them are, in fact, smaller volume accounts that carry no interest rate, justifying our decision to apply an assumption for non-interest bearing accounts at the subtotal level. This frees us up to concentrate our efforts on the few, larger-volume accounts that are interest bearing.

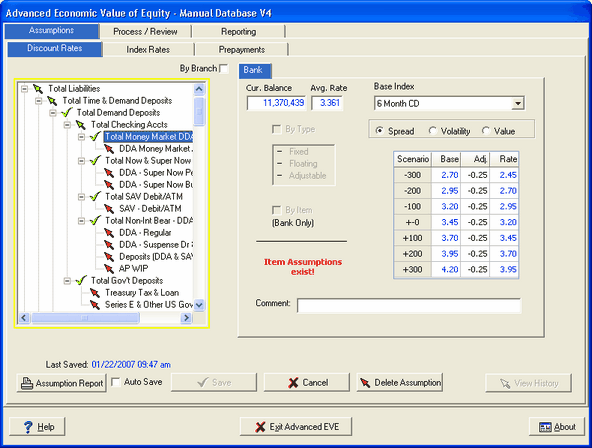

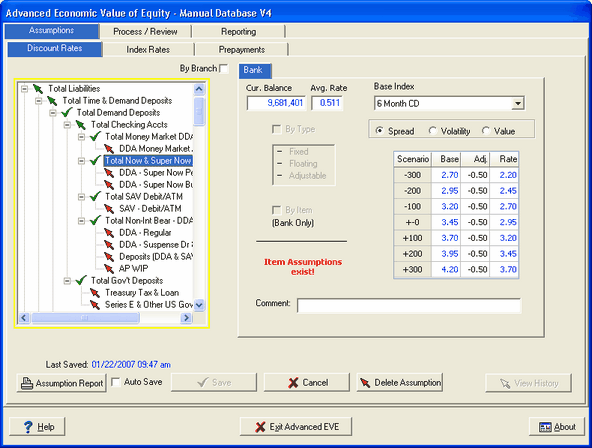

Since NOW accounts do carry an interest rate, we generally do not mark them down from the CD rate as much as the non interest-bearing accounts. We will override the assumption from "Total Demand Deposits" and create an assumption 50 basis points below the 6 MONTH CD index, as seen below:

Money market deposits tend to be more sensitive to market conditions, such as the level of interest rates, than do other demand deposits. Thus, we will override the assumption from "Total Demand Deposits" and create an assumption 25 basis points below the Fed Funds index, as seen below:

We have now very easily and effectively entered discount rate assumptions for all of our demand deposits.