Any item that generates earnings or incurs costs to your institution will require a discount rate in order to generate a proper and reasonable present value under the various rate shocks. For the sake of efficiency and effectiveness, you will want to spend most of your time and energy on the most significant accounts and items. At the same time, for the sake of efficiency, you may not want an assumption on every single account or item, many of which have current balances that are not significant in comparison to the size of the total loan, investment, or deposit category.

The most effective approach is to set a "general" assumption, usually set at a subtotal level, that will apply to those numerous smaller loan or deposit accounts, knowing that you will then go in and make more specific assumptions for the more significant accounts or items. With loans in particular, this concept is important given that the numerous smaller loans will generally be associated with the "less profitable" customers. They will thus likely pay a different, higher rate of interest than will your more profitable, "prime" customers.

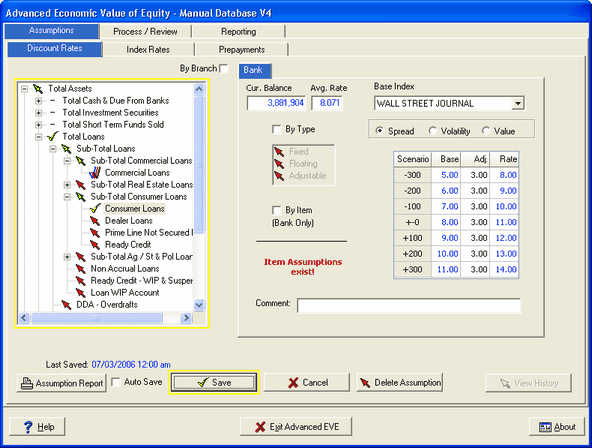

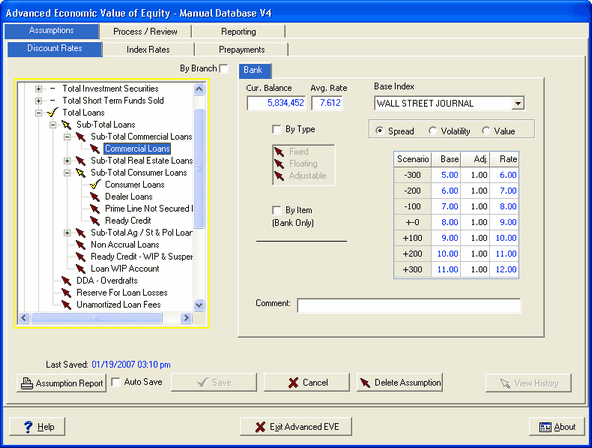

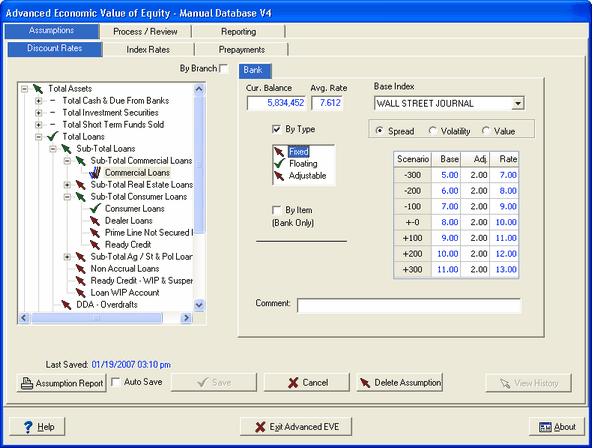

"Total Loans" Assumptions

This is where the real benefit from the "inheritance" of assumptions comes into play. For instance, you can make a generalized assumption at the "Total Loans" level that will flow down to every single account and item that subtotal into "Total Loans". Every loan account has an assumption for discount rates. You can then go into the most significant specific accounts or items, and make more detailed assumptions tailored to those accounts or items.

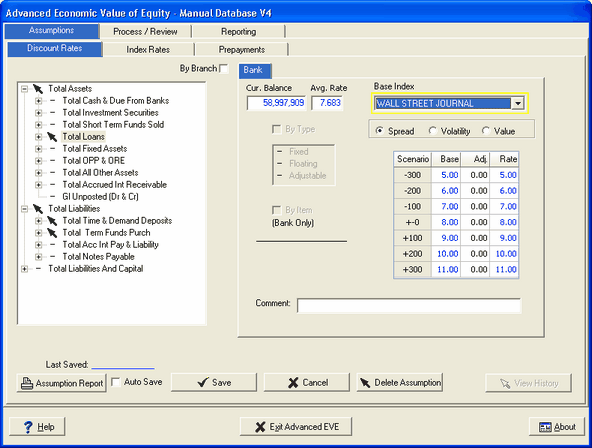

Make your generalized assumption for "Total Loans" first. Remember, this will be the general assumption targeting the numerous smaller loans in the portfolio. In this case, based upon discussions with the ALCO committee and the loan department, along with research of the loan database, you find that your typical fixed rate commercial and mortgage loan, on average, is made at Wall Street Journal Rate plus 2%. Rather than having to calculate what that figure would be in the various shock scenarios, you can utilize the index that is set up under the Index Rate assumption tab. With "Total Loans" highlighted, you select the Wall Street Journal Rate index in the Base Index window.

Note that by selecting "Wall Street Journal" as our Base Index, our index assumptions for Wall Street Journal in the various shock scenario have now automatically filled in under the "Base" column in the assumption area and the Spread method has automatically been selected.

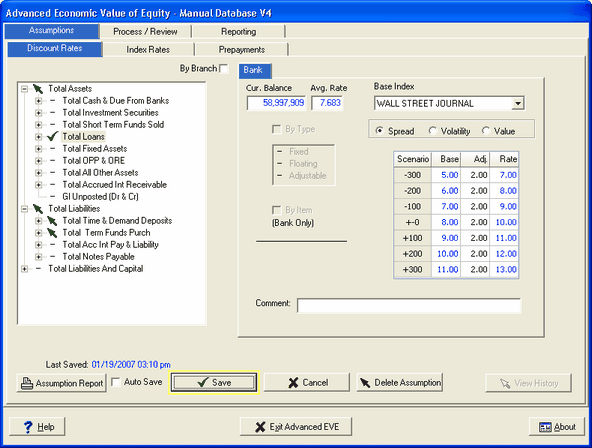

In the screen below we add a 2% spread for all scenarios as our assumption. Note that as you enter your assumption, the rate column is being recalculated.

The assumptions that you have entered here will cause all loans, unless overridden by other assumptions that you will enter, to be valued against Wall Street Journal plus 2% in the respective rate shock environments. In this particular example, in the "no change" shock environment, a loan would be valued against 10.00% (8.00% + 2%). Thus, if the loan in question is on the books at 11%, it would have more value to us in an environment where the same kind of loan would be made at 10.00%, i.e. it would have a gain.

Conversely, if the loan in question was on the books at 9.00%, it would have less value to you in an environment where the same kind of loan would be made at 10.00%, i.e. it would have a loss. In other words, you would rather have the cash in your hands so that you could make the loan at 10.00%. Click the "Save" button to save these assumptions for "Total Loans."

Commercial Loan Assumptions

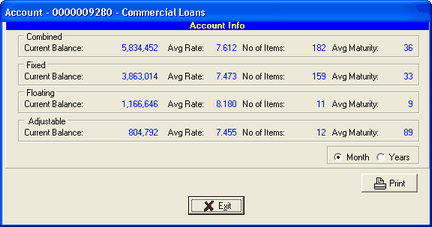

Look at some of the accounts that subtotal into "Total Loans." You have highlighted the account "Commercial Loans", which is the first account with significant enough volume to review and consider separate assumptions than those we inherited from the Total Loans account.

Use the Account Information Tools (right click on an account) to help you determine the assumptions to make. Based on discussions with the loan department and the ALCO committee, you know that the spread for the typical fixed rate Commercial Loan is 2.00% over Wall Street Journal, the same assumption that we made at the subtotal level for "Total Loans."

The Account Information Tools aid displayed below indicates the same information. The Floating Rate Loans, which make up about 20% of the account volume are shown as having priced approximately 1.09% above the Fixed Rate loans. You confirm this information with sources in the institution and determine that the floating rate loans are typically being priced at the current prevailing Prime Rate. You choose to apply a separate assumption to only the Floating rate loans in this account.

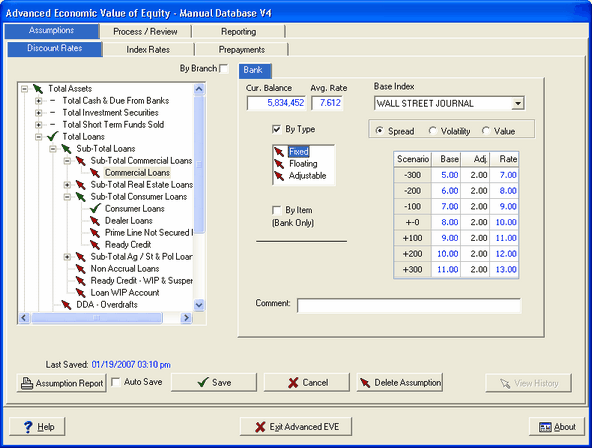

To split the assumptions by type (Fixed, Floating, or Adjustable), click the By Type box:

This enables access to the buttons associated with fixed, floating, and adjustable instruments in that account. Select the Floating radio button and enter the Base Index assumption of Wall Street Journal with no spread entered in the Adj. column.

Note that the "up" arrow has changed to a green check mark ![]() , signifying that the discount rate assumption for floating rate commercial loans now originates here rather that from an account above.

, signifying that the discount rate assumption for floating rate commercial loans now originates here rather that from an account above.

Note that there is now a triple, three colored check mark ![]() next to the account "Commercial Loans" in the General Ledger tree structure. This indicates that one or more discount rate assumptions for this account have been set at the type level.

next to the account "Commercial Loans" in the General Ledger tree structure. This indicates that one or more discount rate assumptions for this account have been set at the type level.

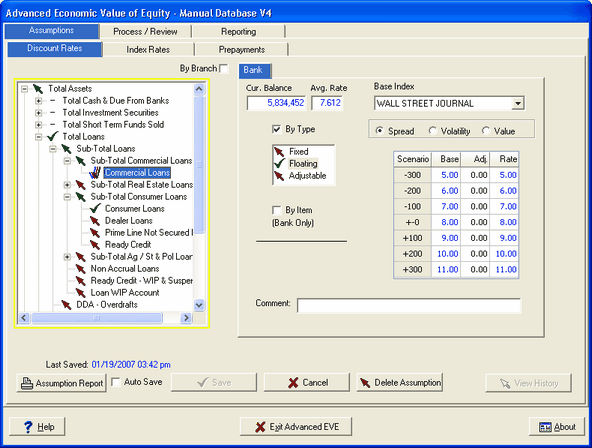

As noted, in the example we have been following, we are using the general assumption that the typical commercial loan is fixed at a rate 2.00% over Wall Street Journal. We handled one set of exceptions, floating rate commercial loans, by setting their discount rate assumptions at the type level.

We also want to be able to set specific discount rate assumptions for significant individual fixed rate loans that may tend to price differently than our typical loan. For instance, as we noted earlier, "prime" customers tend to get better terms on their loans, including lower rates. Loans such as these should have different discount rate assumptions.

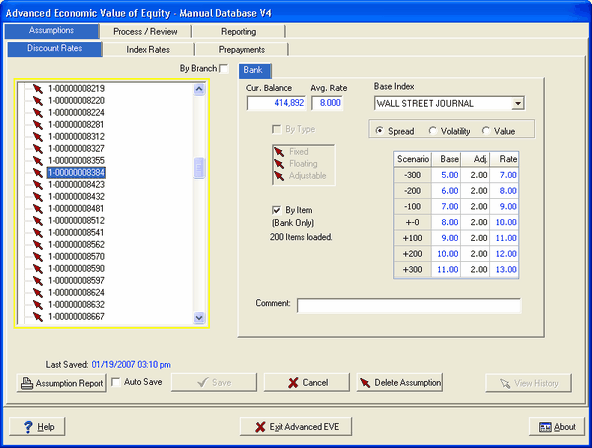

To implement assumptions for individual fixed rate loans, click on the account in the General Ledger tree structure (left side of screen.) Then, with the By Type enabled and the radio button selected next to Fixed, check the By Item section of the screen:

This closes the tree view screen above and opens the item display, as seen below, in its place. This gives you access to assumptions for items in the "Commercial Loans" account on an individual loan basis.

In the screen above under By Item, we see the total number of items loaded for this type, commercial fixed rate loans. There are several sizable loans that price at spreads lower than the typical commercial fixed rate loan, but for the purposes of illustration, we will concern ourselves with just one example.

Loan number "8384" is a $414,892 loan at a yield of 8.00%, which was 1.00% below prime when it was originated for a long-time, favored customer.

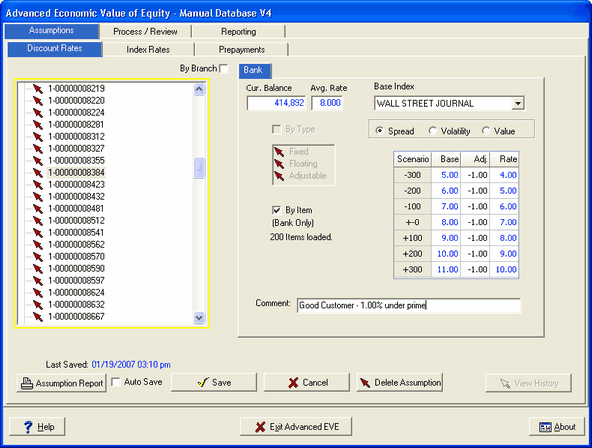

To make the assumption for this particular loan item, we will assume that a similar loan to the same good customer would be made under similar terms, 1.00% under prime rate. Thus, we input that assumption and click "Save" as seen below:

In the current rate shock environment (+/- 0 scenario), we are valuing loan number "1299654," which is on the books at 8.00%, against a discount rate of 7.00% (Current prime- 8.00%, less the 1.00% spread).

After processing, our results for this specific loan would show a gain in the current rate shock environment. In other words, it is obviously more valuable to us to have the funds already loaned out at 8.00% than to be faced with having to make the same loan today at 7.00%.

Conversely, in the "+ 300" rate shock scenario, our results will show a loss. This is because we will already have the funds loaned out at 8.00% when we could make the same loan today, following an immediate 300 basis point jump in rates, at 10.00%.

All of the other loans in the "Fixed" type under the "Commercial Loans" account will continue to get their discount rate assumptions from the parent account, "Commercial Loans," which in turn is getting its assumptions from "Total Loans."

And the loans in the "Floating" type under the "Commercial Loans" account will continue to get their discount rate assumptions from the "Floating" type level. To return to the General Ledger tree structure display, uncheck the box next to By Item. As long as you clicked the "Save" button after entering the assumptions for each item, those assumptions will remain saved after you disable By Item.

Installment Loan Assumptions

Installment or Consumer Loans typically have higher rates of interest associated with them in order to compensate for the perceived higher level of risk and the higher costs involved in processing those loans. In our example, the loan department has indicated that the typical Consumer Loan is made at 3.00% over prime. The volume of Consumer Loans in the example institution is sufficient to justify a specific discount rate assumption as shown below: