With the exception of savings accounts, setting discount rates for time deposits is a very similar process as that for loans. The interest rate that we would pay for that deposit in the various rate environments will be the appropriate rate at which to discount the deposit in that environment.

In other words, if we would make a six-month CD under $100M at 4.0% in a down 100 basis point shock scenario, then that would be the appropriate rate at which to discount that particular CD. Savings accounts, because they have no specified maturity, and because they tend to be low-cost, stable deposits, are treated in much the same way as demand deposits in setting their discount rates.

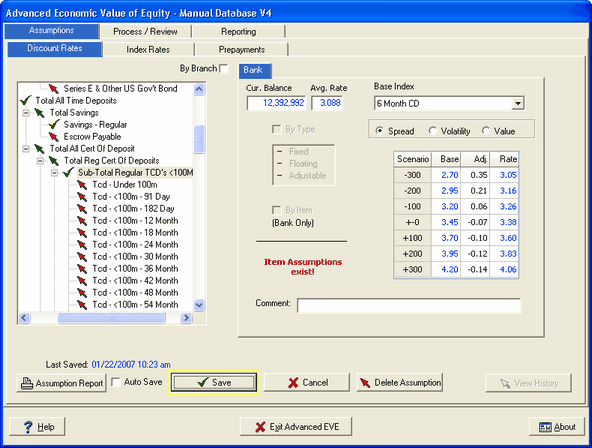

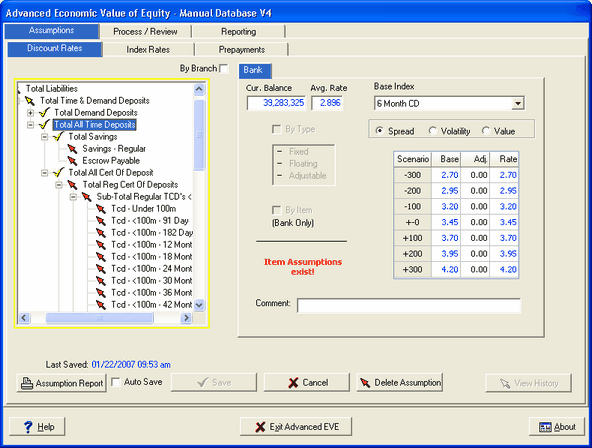

Since we will use our 6 MONTH CD index to set the discount rate assumptions for all time deposits, let's go ahead and set that assumption at the subtotal level, as seen below, and then we will open the account structure in order to access the various time deposit accounts.

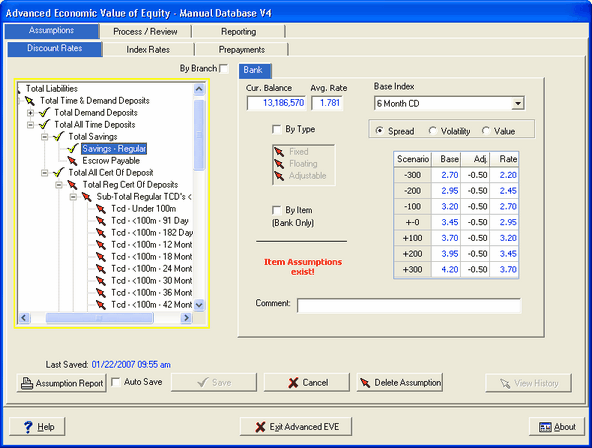

Savings accounts tend to be relatively insensitive to market conditions, such as the level of interest rates, compared to other demand deposits. Furthermore, the depositor cannot write checks against the account, making it relatively illiquid and, thus, a more stable funding source for the institution. Thus, we will override the assumption from "Total Demand Deposits" and create an assumption 50 basis points below the 6 MONTH CD index, as seen below:

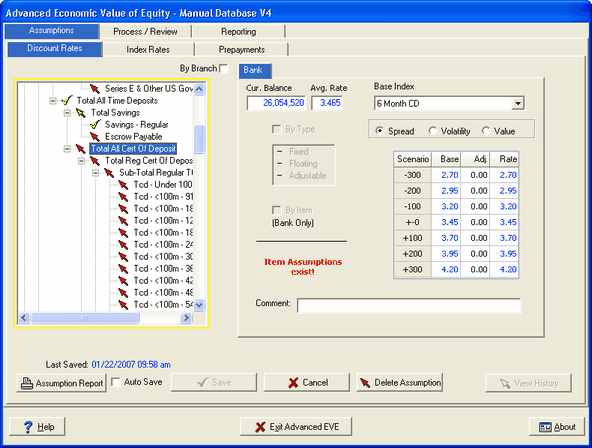

As in previous examples, we will let our generalized assumption apply to the smaller, less significant accounts and we will devote our attention to the larger volume accounts. We move down to the "Total All Cert of Deposit" account, our regular CDs in this particular institution.

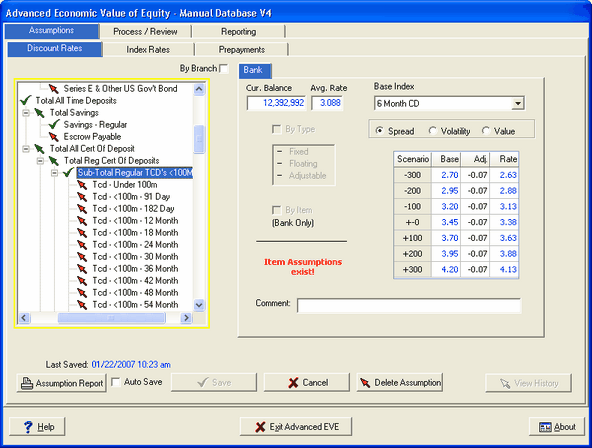

We already have the six month CD set up as an assumption, inherited from the parent "Total All Cert of Deposit" account. And while the majority of CDs may originate as six-month maturities, we need to consider whether enough other CDs originate in other maturities at sufficiently different rates to justify marking up or down from the 6 MONTH CD index.

For example, in this particular institution, we know that while 50% of CDs originate as six-month maturities, 30% originate as three-month CDs and another 20% originate as twelve-month maturities. Currently, the three-month CD prices at 3.00% and the twelve-month CD prices at 3.80%. Thus, the weighted average cost of a current CD would be 3.39% ((3.00% * .3) + (3.45% * .5) + (3.80% * .2)).

Thus, we mark the discount rate for the "Sub-Total Regular TCD's <100M" account down from the 6 MONTH CD index, in this case by .07% (3.45% - 3.39%):

That would be the simplest approach to setting discount rates for CDs. However, in order to achieve a more accurate valuation, we might want to consider how the spread between the three-, six-, and twelve-month CD rates might change as interest rates change. Many factors might influence this spread, but one approach might be that we would be more likely to encourage depositors to select longer maturities when rates are low, thus widening the spread by providing more premium for longer-term CDs, and more likely to want them to select shorter maturities when rates are high, thus narrowing the spread by decreasing the premium for longer-term CDs. In other words, we would be happy to have longer-term CDs on our books at low rates, but not at higher rates.

By keeping an historical database of offered CD rates, and even tracking the flow of funds into the various maturities, one can develop a good idea of how to value the CDs in relation to the underlying index, in our example the 6 MONTH CD. In our example, we found that at the low extreme in rates, the institution offered a sizable premium for 12-month CDs, leading to a weighted average rate of 3.05% for new CDs, which is 0.35% over the 6 MONTH CD index at -300 basis points.

At the high extreme in rates, the premium narrowed considerably, reducing incentives for depositors to go long. Thus, when rates were extremely high, the CD rate schedule was fairly flat and more depositors opted for shorter-term CDs, leading to a weighted average rate of 4.06% for new CDs, which is 0.14% below the 6 MONTH CD index at +300 basis points. Between the current spread and the spreads at the extremes, we adjust the spread incrementally as shown below: