![]() Main Menu | Reporting | My Reports | Select Group Filer (Advanced Inc. Shock) and Edit

Main Menu | Reporting | My Reports | Select Group Filer (Advanced Inc. Shock) and Edit

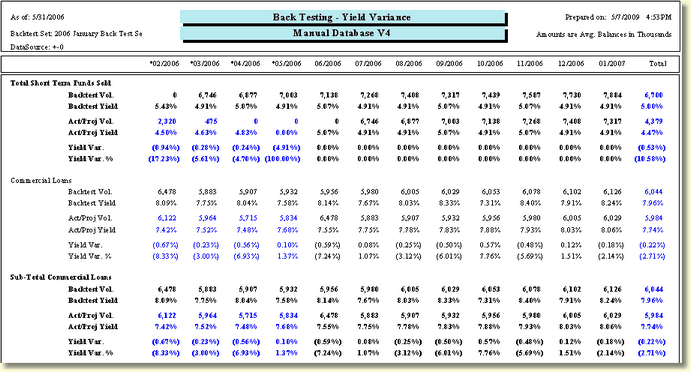

The Back Testing Financial Statement Variance report provides a view of balances,associated yields, and variances for the balance sheet with a comparison between the selected default Back Test set and Historical and Current Projections. Reports can be configured for each of the seven shock scenarios; by default the ±0 is setup in the model. Also, Average / Ending balances can be selected.

The report is based on the Chart of Accounts and will show all historical months in blue and for non-color printers with an asterisk-* in the date column headers.

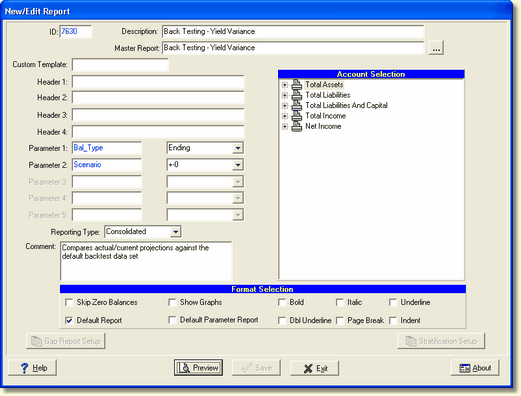

The following screen displays the system parameters that can be customized by the bank.

There are two system parameters for this report which can be changed by the user:

Parameter 1: Bal_Type - Select Average(Avg.) or Ending(End.). This parameter pertains to the balance sheet side of the General Ledger. The Income side will always use ending balances. The report will print which balance type you have selected in the upper right hand area, below the date columns.

Parameter 2: Scenario - The default scenario is +-0. Seven shock scenarios are available. If you change this parameter, you may need to change the header to show the appropriate scenario you're using. The report also displays the data source in the upper left hand corner which shows the scenario used for the report.

Calculations

Actual data is shown in blue; projections are shown in black.

The yields calculated are based upon the interest basis of the items contained in the account as well as the reinvestment calculated on an Actual/Actual interest basis by default.

The yield basis of an account can be set in the Parameter Setup / Chart of Accounts section and will then override the default interest basis for reinvestments.

The Total column is a simple average of the 12 month yields.