The Prepayments tab can be accessed in each of the 2 modules. Below are the paths to access PrePayments.

![]() Main Menu | Advanced Income Shock | Assumptions | PrePayments

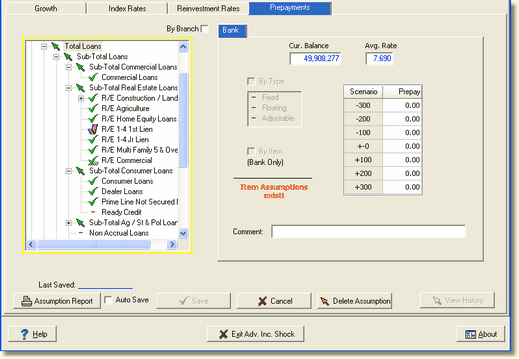

Main Menu | Advanced Income Shock | Assumptions | PrePayments

![]() Main Menu | Advanced EVE | Assumptions | PrePayments

Main Menu | Advanced EVE | Assumptions | PrePayments

Certain loans and investments, particularly mortgages and mortgage-backed securities, are subject to prepayments of principal. For these items, portions of the principal are paid earlier than expected based upon the terms of the contract, which increases the speed of the cash flow and shortens the life of the item. This also possibly reduces the number of periodic interest payments on the item. Thus, we should make prepayment assumptions on accounts that are assumed to be affected by the possibility of such prepayments.

While prepayments are typically associated with refinancing's on mortgages, virtually any kind of loan can be prepaid or refinanced. Borrowers will usually refinance when interest rates have fallen sufficiently below the current rate on their loans that it will be beneficial to them in terms of reduced periodic payments, or reduced total payments over the life of the debt.

For the lender, prepayments represent a "double-edged sword." Prepayments represent accelerated cash flow, which tends to increase the present value of the loan. However, because prepayments typically accelerate during low rate environments, this cash flow is being returned to the lender at a time when it will likely be difficult to reinvest at a comparable interest rate without extending maturities.

When rates rise, prepayments tend to slow as it becomes less and less advantageous to pay off debt. There is obviously little incentive for a borrower to pay off his loan or his mortgage if a new loan or mortgage is going to cost more, i.e. when market rates are higher than the current rate on loans. For all of these reasons, we tend to see prepayment rates increase as rates fall and to see them slow when rates increase.

Though it is a less common and less significant occurrence, "prepayments" can occur on CDs. Such an event would occur when a depositor redeems his CD earlier than the stated maturity. Financial institutions typically write an "early withdrawal" penalty into the CD contract, usually costing the depositor several months interest to redeem the CD early. While it is relatively rare, depositors would generally be inclined to redeem a CD early when rates have risen sharply higher, sufficiently to offset the cost of the "early withdrawal" penalty.

There are a number of places one can obtain information on the impact of changing interest rates on mortgage prepayments. The best place to start is with your institution's loan department and loan officers. Other sources of information might be found on websites for the various Federal Reserve banks and the various agencies involved in the housing market. Also, investment brokerages often have information pertaining to prepayments on mortgages and mortgage-backed securities.