Non Interest Bearing DDA accounts do not require a repricing assumption.

Pricing assumptions in the Deposit area can vary depending upon how an institution has arranged its General Ledger. Typically, several indices will be maintained on the host system as basis for pricing various types of deposit funds.

If an institution arranges its General Ledger where an account contains only items tied to a particular index, the assumptions are very simple. All one has to do is tie the account to the base index. Typically, the base index has already been configured to represent the pricing assumptions in the alternate scenario.

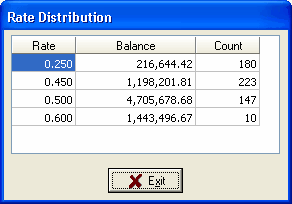

However, very commonly, items with different pricing categories are mixed into the same account. For our first sample account, we use the Rate Distribution option in the Account Information Tools to examine our item distribution.

We can see from the rate distribution, that the account is divided between four major volume groups that are paying four different rates. The system, when computing a re-pricing volume, will not make any distinction between the various rate groups. Therefore, the re-pricing assumption should be based upon an average rate between all the groups.

The best source is the weighted average rate on the account. However, this weighted rate is based upon your current volume. If you foresee a significant change in the mixture of items in the account, you may have to determine your own average rate for your pricing assumption.

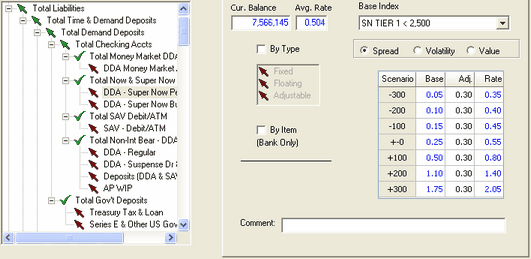

To maintain the principle of tying assumptions to an index whenever possible, we chose one of the SUPER NOW account indices. We then determine an appropriate spread that will arrive at our intended pricing assumption. As you can see, the base index SN Tier 1 <2,500 is setup to not move in parallel with the shock scenario assumptions. This is very typical in the deposit area of the balance sheet.

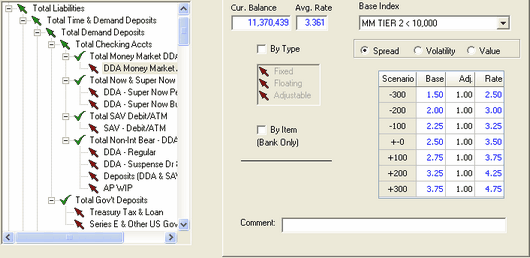

We followed the same thought process on our next sample account, DDA Money Market. We examined the rate distribution, but referred back to the Average weighted account rate for the basis of our assumption. Again, we use one of the indices used in the account as the basis for our assumption. This provides us with the appropriate assumption behavior in the alternate shock scenarios.

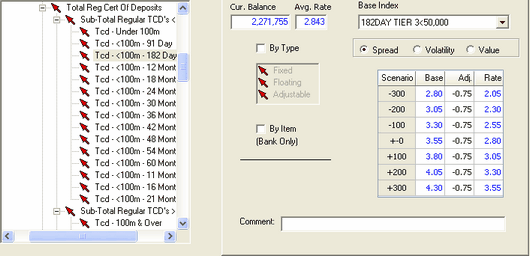

For the time deposit accounts, pricing is largely influenced by the contractual amount of time an item is being deposited in the institution as well as the volume of the item. Again, the system will not make any distinction in the reinvestment amount based upon those criteria's. Therefore, you have to choose an average rate for your reinvestment assumption. We use the average weighted rate in the account as your guide since we projected no significant change in the mixture of items in the account.

You use one of the host CD Indices as a basis for the assumption. This provides the mechanism of following the index assumption with your spread and making the alternate scenario assumptions primarily with the index.

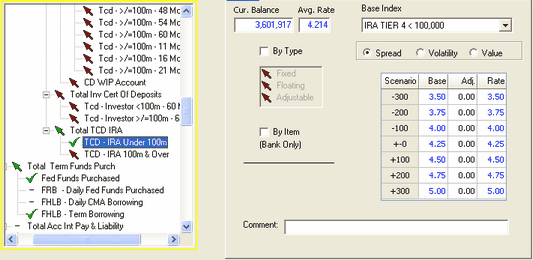

The last account in our sample institution, TCD - IRA Under 100m, has a base host index that guides the pricing of items in this account.

We therefore simply tie the reinvestment assumptions to the host index.